What Startups Miss About Banks

Lessons from Both Sides of the Table

I used to think banks were just slow. When I was pitching mobile payments to bankers years ago, I couldn't understand why they didn't see what seemed obvious to me. Working inside a bank, I've had to revisit some of those assumptions.

This isn't a defense of bad user experiences or outdated systems. Banks have real problems. But the way I used to think about those problems, and the solutions I imagined, missed some fundamental things.

How I Used to Think

When you're building products and pitching them to banks, you develop a mental model of why they're the way they are. Mine went something like this: banks are slow because they're old, bureaucratic, and resistant to change. If someone would just build a better experience, clients would flock to it. The bundle of services banks offer could be broken apart and rebuilt by companies focused on doing one thing well.

I wasn't alone in thinking this way. A lot of people in tech believed some version of it. And parts of it were true. Fintechs did build better experiences for specific problems. But I was missing the bigger picture.

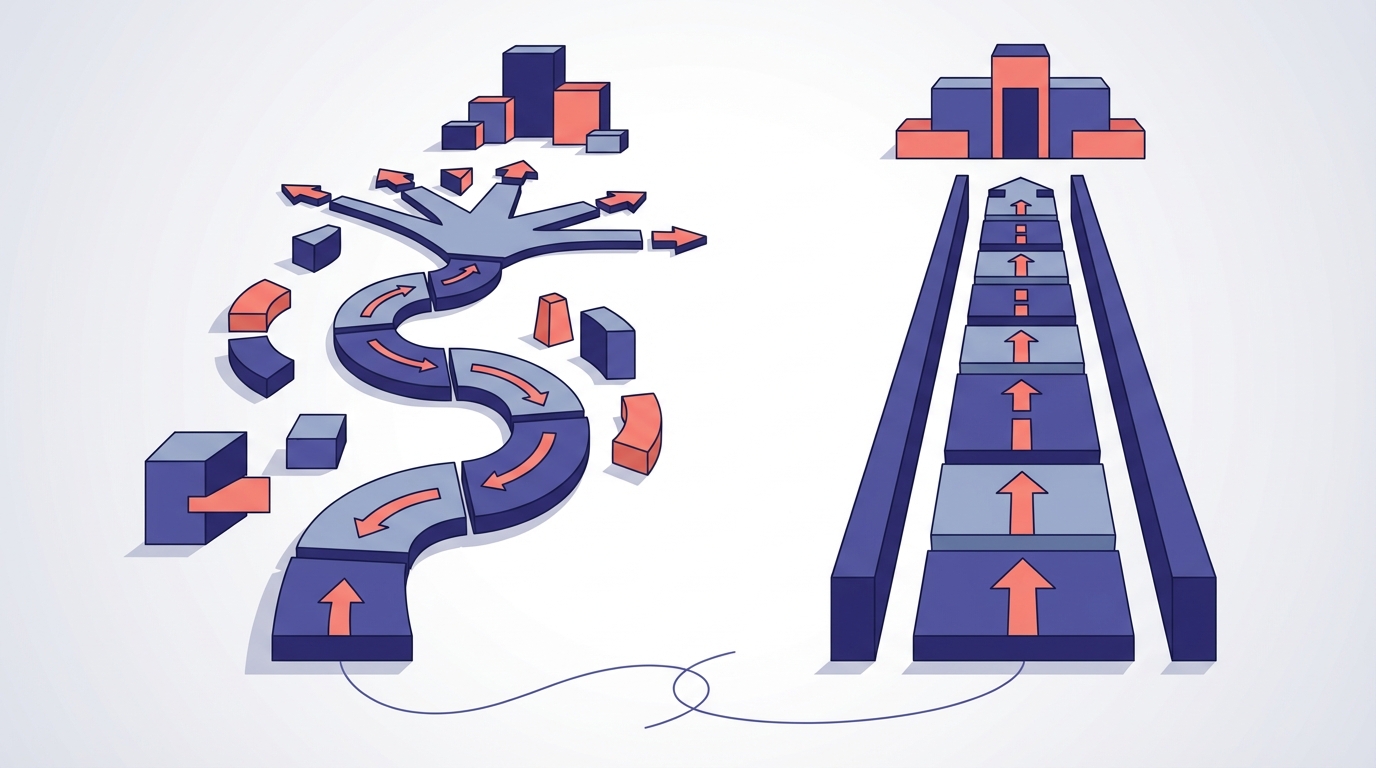

Permissive vs. Restrictive

The thing that clarified my thinking was understanding how differently corporations and banks are set up to operate.

Most companies work under what you might call a permissive framework. They can do anything not explicitly prohibited by law. Want to launch a new product? Figure out the legal guardrails and go. The bias is toward action.

Banks work under a restrictive framework. They can only do what is explicitly authorized. Every product, every service, every significant change has to fit within a regulatory structure that spells out what's allowed. The bias is toward caution, with compliance as the starting point.

This difference explains a lot. When I was on the outside trying to move fast, I was operating under one set of rules. The banks I was pitching were operating under a completely different set. What looked like resistance to change was often a reasonable response to constraints I didn't fully see.

Regulation

I knew regulations existed when I was pitching banks. I didn't appreciate how much they shape every decision. KYC, AML, BSA, CRA, UDAAP, Reg E. Each one comes with specific requirements, examination schedules, and consequences for getting things wrong. The framework is comprehensive, and that comprehensiveness is part of what makes the banking system trustworthy.

The same compliance discipline is required of every chartered institution, regardless of size. The rules apply whether a bank has $500 million in assets or $500 billion, which means the operational cost of compliance is a larger relative load on smaller institutions. That dynamic shapes what community banks can do and the pace at which they can do it, in ways that aren't visible from the outside.

A startup serving a narrow client segment can optimize for that segment. A bank has CRA obligations to serve its entire community, including clients who aren't profitable. A startup can choose not to serve certain geographies or client types. A bank's charter comes with responsibilities that don't get shed.

Trust

There's also something harder to quantify. Banks hold people's money. That creates a relationship built on decades of trust, not months of marketing. Community banks often have multi-generational client relationships. Families have banked at the same institution for generations.

Fintechs compete on features and experience, which matters. But when something goes wrong with a fintech account, clients navigate support tickets and chat interfaces. When something goes wrong at a community bank, there's often someone who knows the client and can make it right.

I'm not romanticizing this. Some of that personal touch masks inefficiency. But there's a reason people trust their money to institutions that have been around for decades. That trust was earned, and it doesn't transfer easily to a new app.

What I Got Wrong

I underestimated structural constraints. When banks passed on my pitches, I assumed they just didn't get it. Sometimes that was true. But often it was a reasonable assessment of regulatory risk, integration complexity, or priorities I couldn't see from where I sat.

I overestimated how much better UX alone could solve. A beautiful interface doesn't help if the underlying product doesn't meet actual needs, or if the economics require fees that erode the experience.

I didn't appreciate the value of having everything in one place. The idea of breaking apart banking services assumes clients want separate apps for each financial need. Some do. But many prefer the convenience of a single institution that handles checking, savings, lending, and more.

What I See Now

I see both perspectives more clearly now. Banks have real problems with technology, data, and client experience. The critiques weren't wrong about that. But the solutions are harder than building a better app. The regulatory environment, trust dynamics, and business model constraints make this genuinely complex.

I'm excited about the work ahead. The opportunity to use data and technology to improve community banking is real. But the work has to operate within these constraints, in close collaboration with the regulators who help define them, not in opposition to them.