Exploring Mortgage Lending Data

Putting the Tools to Work on Real Data

With Jupyter, pandas, and matplotlib set up, let's put those tools to work on real data.

The Data

I'm using publicly available HMDA data, which stands for Home Mortgage Disclosure Act. Since 1975, most mortgage lenders in the US have been required to report detailed information about their lending activity. The Consumer Financial Protection Bureau publishes this data annually, and anyone can download it from ffiec.cfpb.gov/data-browser.

For community banks, HMDA data matters. Regulators use it to assess whether banks are serving their communities fairly. It feeds into CRA (Community Reinvestment Act) examinations. It reveals lending patterns across geography, loan types, and borrower demographics. Understanding how to work with this data is directly relevant to the regulatory environment banks operate in.

I downloaded 2021 data for Pennsylvania to keep the file size manageable. The full national dataset runs into tens of millions of records. Pennsylvania is a good pick because the Philadelphia metro area is one of the largest mortgage markets on the East Coast, and the state has enough geographic diversity to make the analysis interesting.

Loading and First Look

import pandas as pd

import matplotlib.pyplot as plt

df = pd.read_csv('hmda_2021_pa.csv')

print(f"Records: {len(df):,}")

df[['activity_year', 'loan_type', 'loan_purpose', 'loan_amount',

'action_taken', 'state_code', 'county_code', 'income']].head()

Records: 863,993

activity_year loan_type loan_purpose loan_amount action_taken state_code county_code income

0 2021 1 32 75000 1 PA 42101 159

1 2021 1 32 175000 1 PA 42133 131

2 2021 1 31 215000 4 PA 42077 150

3 2021 1 1 235000 4 PA 42101 45

4 2021 1 31 95000 4 PA 42133 130

Nearly 864,000 loan records from one state in one year. The columns use numeric codes rather than labels. Loan type 1 is conventional, 3 is VA. Loan purpose 1 is purchase, 31 is refinance. Action taken 1 means the loan was originated. The county_code field uses standard FIPS codes from the Census Bureau, so 42101 is Philadelphia County. The CFPB publishes a complete data dictionary with every field definition and valid code value, which is worth bookmarking if you plan to work with this data.

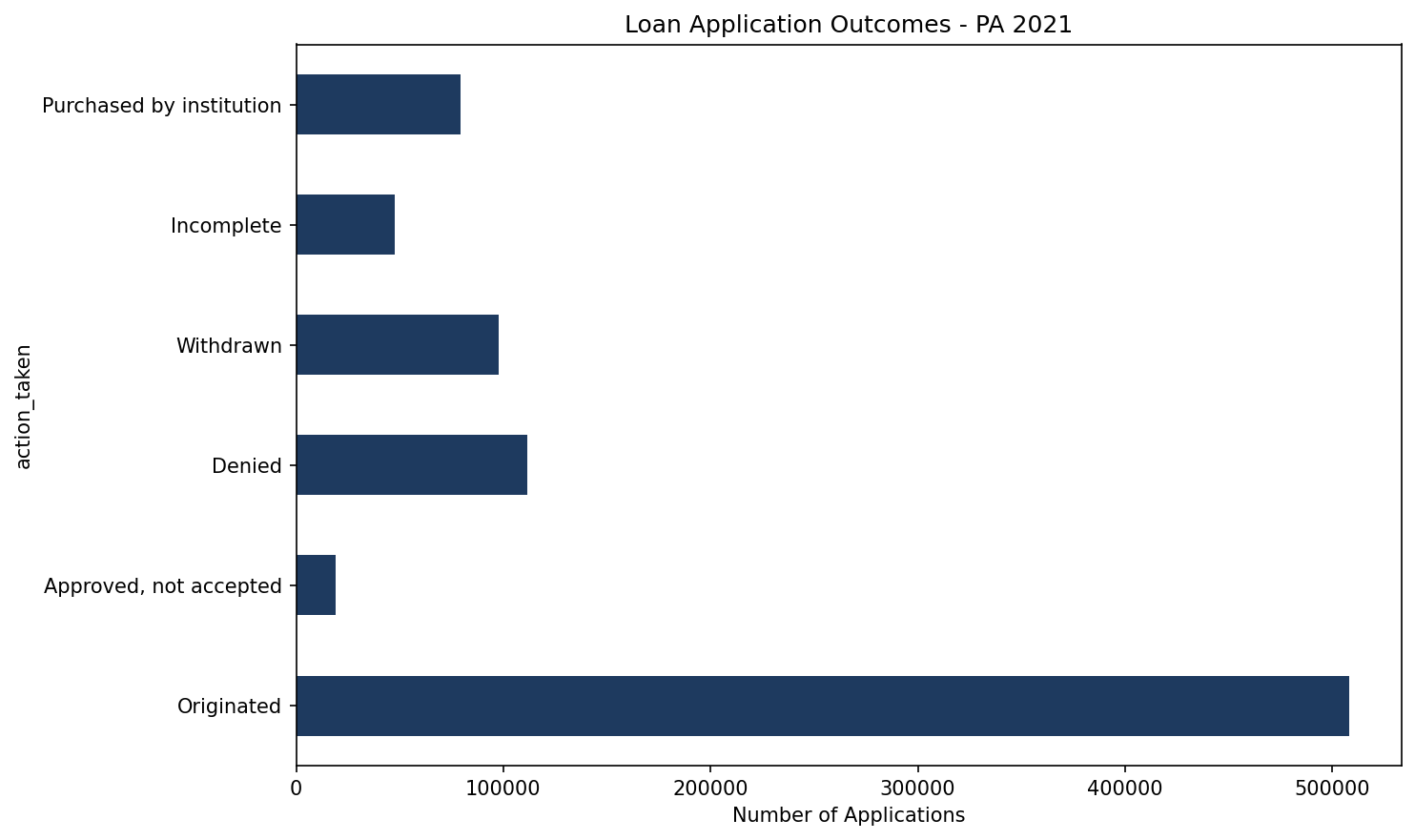

What Happened to These Applications?

The action_taken field tells us the outcome of each application.

action_counts = df['action_taken'].value_counts().sort_index()

action_labels = {

1: 'Originated',

2: 'Approved, not accepted',

3: 'Denied',

4: 'Withdrawn',

5: 'Incomplete',

6: 'Purchased by institution'

}

action_counts.index = action_counts.index.map(lambda x: action_labels.get(x, f'Other ({x})'))

action_counts

Originated 507,990

Approved, not accepted 18,948

Denied 111,574

Withdrawn 97,634

Incomplete 47,643

Purchased by institution 79,262

About 59% of applications resulted in originated loans. Another 13% were denied. What caught my eye is that denials outnumbered withdrawals. I half expected the opposite during the 2021 refi boom, when people often shop several lenders at once and let the extra applications lapse. When the data doesn't match your hunch, that's usually where the interesting questions start.

action_counts.plot(kind='barh', figsize=(10, 6), color='#1e3a5f')

plt.title('Loan Application Outcomes - PA 2021')

plt.xlabel('Number of Applications')

plt.tight_layout()

Loan Types and Amounts

How do conventional loans compare to government-backed loans?

loan_type_labels = {1: 'Conventional', 2: 'FHA', 3: 'VA', 4: 'USDA'}

df['loan_type_name'] = df['loan_type'].map(loan_type_labels)

df.groupby('loan_type_name').agg({

'loan_amount': ['count', 'mean', 'median']

}).round(0)

count mean median

loan_type_name

Conventional 711,919 225,032 175,000

FHA 96,556 187,207 165,000

USDA 7,163 162,225 155,000

VA 48,355 243,566 215,000

Conventional loans dominate at 82% of volume. VA loans average $243,566, close to conventional, reflecting the purchasing power of military borrowers. FHA and USDA serve lower price points at $165,000 and $155,000 median respectively, fulfilling their mission of expanding homeownership access. The relatively small USDA count makes sense for Pennsylvania, where eligible rural areas are limited compared to more agricultural states.

Denial Rates by Loan Type

This is where it starts to get interesting. Are denial rates consistent across loan types?

# Filter to just applications (not purchases)

applications = df[df['action_taken'].isin([1, 2, 3, 4, 5])]

# Calculate denial rate by loan type

denial_by_type = applications.groupby('loan_type_name').apply(

lambda x: (x['action_taken'] == 3).sum() / len(x) * 100

).round(1)

denial_by_type.sort_values(ascending=False)

loan_type_name

FHA 14.5

Conventional 14.3

VA 13.2

USDA 7.9

dtype: float64

FHA has the highest denial rate at 14.5%, which fits, since these borrowers typically have lower credit scores and less saved for a down payment. What I didn't expect is how close conventional sits at 14.3%, just 0.2 points behind. I'd have guessed a wider gap between the two. USDA remains the lowest at 7.9%, likely because those loans go through pre-qualification before a formal application.

Raw denial rates only tell part of the story. The real question is whether those rates vary by borrower demographics, which is where fair lending analysis begins.

Geographic Patterns

Which counties have the most lending activity?

county_activity = df[df['action_taken'] == 1].groupby('county_code').size()

top_counties = county_activity.nlargest(10)

top_counties

county_code

42003 51,395

42101 47,274

42091 44,197

42017 34,071

42029 30,307

42045 24,255

42071 22,166

42133 22,015

42011 16,084

42077 14,880

dtype: int64

County 42003 is Allegheny (Pittsburgh) and 42101 is Philadelphia. Pittsburgh edges out Philadelphia in raw county-level originations. But the Philadelphia story changes when you look at the metro area. Four of the next five counties on the list are Philadelphia's collar counties. Montgomery (42091), Bucks (42017), Chester (42029), and Delaware (42045) together with Philadelphia account for over 180,000 originated loans, roughly 35% of all lending in the state. The Philadelphia metro area is by far the dominant mortgage market in Pennsylvania.

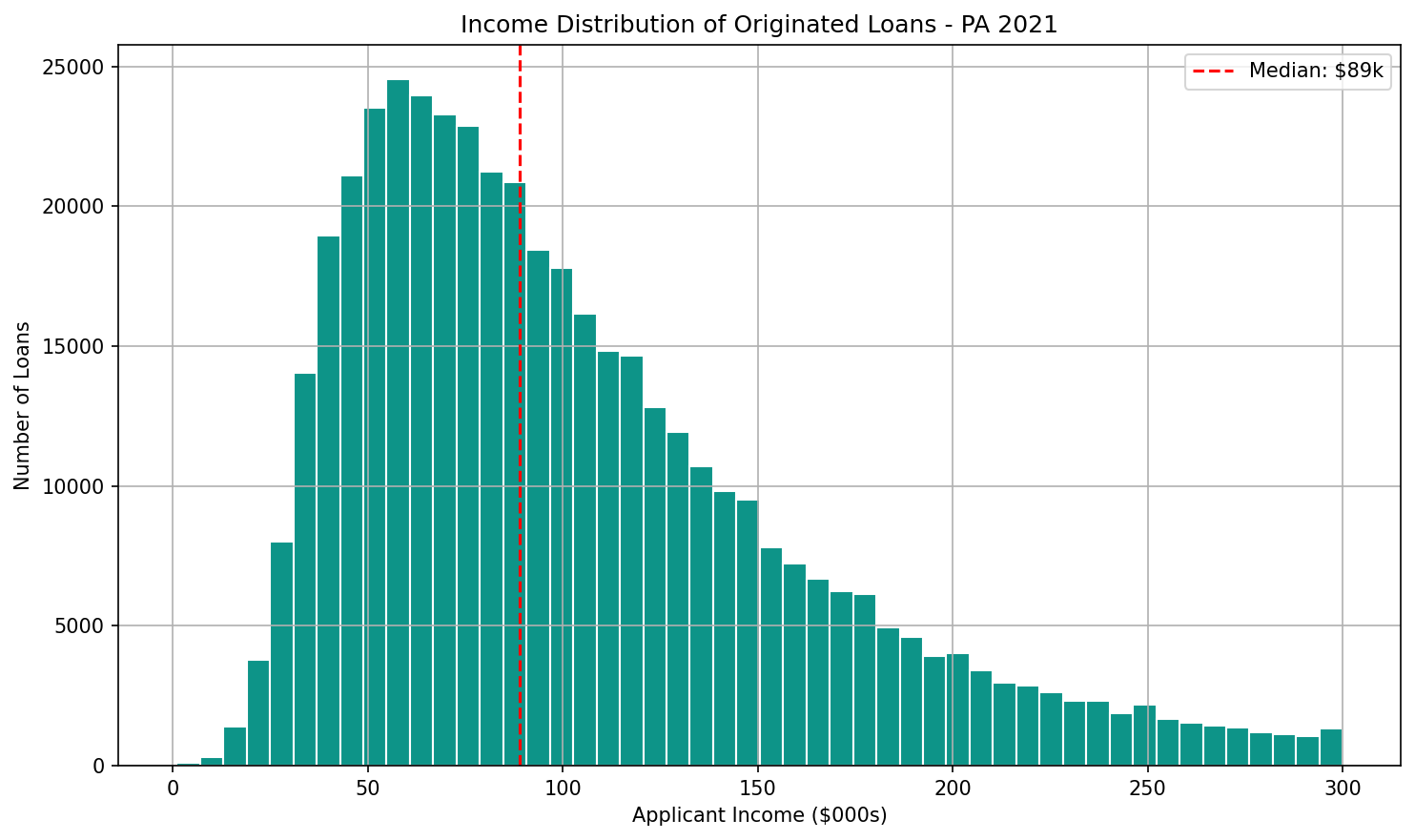

Income Distribution of Approved Loans

What does the income distribution look like for borrowers who actually got loans?

originated = df[df['action_taken'] == 1]

income = originated['income'].dropna()

income_clean = income[(income > 0) & (income <= 300)]

plt.figure(figsize=(10, 6))

income_clean.hist(bins=50, color='#0d9488', edgecolor='white')

plt.title('Income Distribution of Originated Loans - PA 2021')

plt.xlabel('Applicant Income ($000s)')

plt.ylabel('Number of Loans')

plt.axvline(income_clean.median(), color='red', linestyle='--',

label=f"Median: ${income_clean.median():.0f}k")

plt.legend()

plt.tight_layout()

The distribution is right-skewed, with most borrowers earning between $40,000 and $150,000. The median is $89,000. There's a long tail of higher-income borrowers, which is typical for mortgage data and reflects the Philadelphia metro's mix of moderate-income neighborhoods and affluent suburban corridors.

What This Reveals

A single morning with HMDA data surfaces patterns that would take weeks to compile by hand. Denial rates cluster tightly across loan types in Pennsylvania. Lending concentrates heavily in the Philadelphia metro area. Income distributions shift based on how you slice the data.

This is what data exploration looks like in practice. You start with broad questions, run simple aggregations, and let the numbers guide you toward more specific inquiries. Some findings confirm what you'd expect. Others raise questions worth investigating further.

For a community bank, this kind of analysis connects to CRA planning, fair lending monitoring, and plain market understanding. And because HMDA data is public, anyone can benchmark an institution against the broader market using nothing but published records.