Brushing Up on Financial Statements

The Basics Before Reading a Bank's Books

I've been wanting to dig into bank financial statements, but I kept realizing I was fuzzy on some basics. I've worked with financial statements before, built projections for investors, reviewed monthly P&Ls, tracked cash burn. But that was a while ago, and I never had formal accounting training. So before jumping into bank-specific financials, I wanted to ground the fundamentals.

The Three Statements

Every business has three core financial statements, and each one answers a different question.

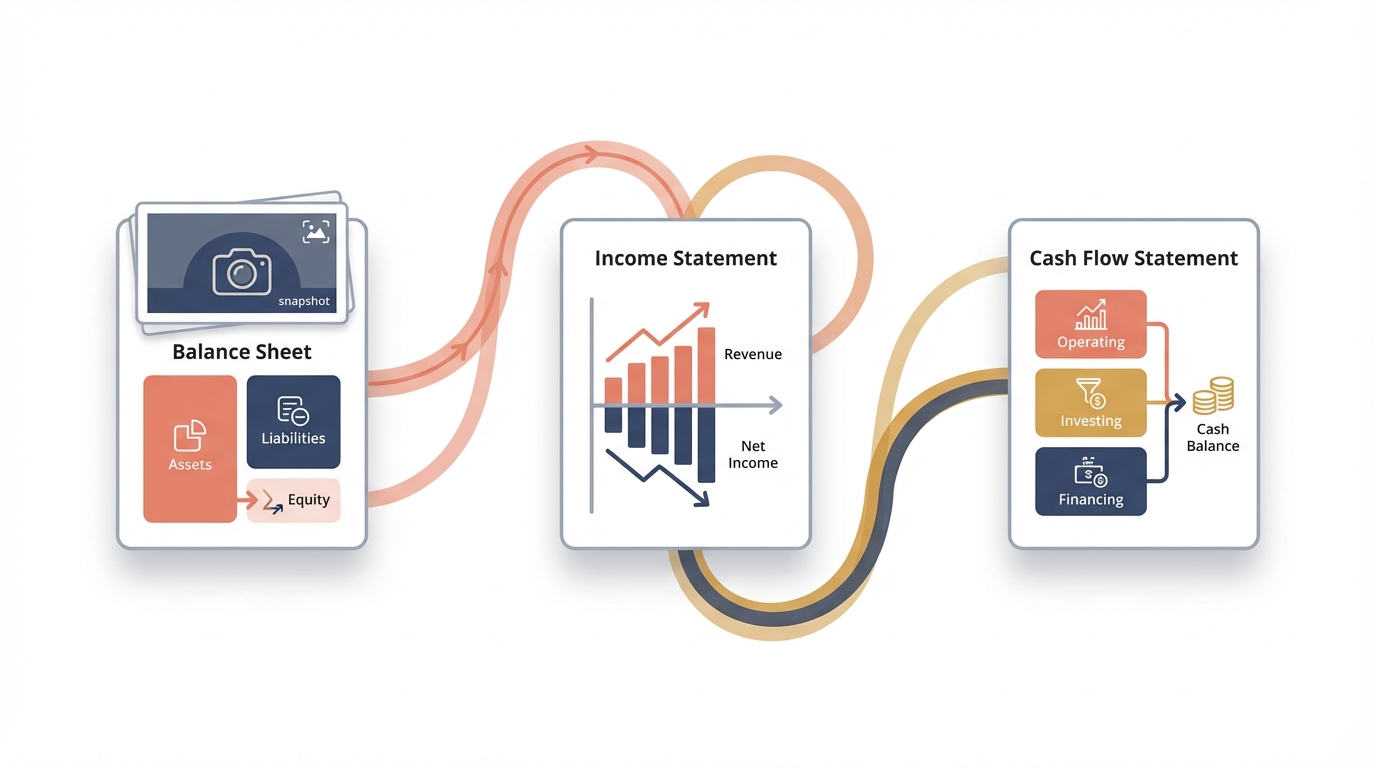

The balance sheet is about position. What does the company own, what does it owe, and what's left? It's a snapshot at a single point in time. The fundamental equation is straightforward. Assets equal liabilities plus equity. Assets are what the company owns, things like cash, equipment, and receivables. Liabilities are what it owes, including loans, payables, and deferred revenue. Equity is the difference, the owners' residual claim on the business.

The income statement is about performance. Did the company make money over this period? It covers a span of time, usually a quarter or a year, and tracks revenue minus expenses to arrive at net income. This was the one I watched most closely when running companies. Revenue growth told me whether we had traction. Operating expenses told me how fast we were burning. The gap between them told me how much runway we had left.

The cash flow statement is about movement. Where did the cash actually go? This one matters more than most people realize. A company can show a profit on the income statement and still run out of cash. Receivables that haven't been collected count as revenue, but they're not cash in the bank. Capital expenditures don't show up on the income statement but they drain cash. The cash flow statement reconciles the difference between accounting profit and actual cash movement.

Stock vs. Flow

One of the most useful distinctions in accounting is between stock and flow. The balance sheet is a stock. It captures a position at a moment in time. Think of it as a photograph. The income statement and cash flow statement are flows. They capture activity over a period. Think of them as a video.

This distinction matters because the two types of statements interact. Net income from the income statement flows into retained earnings on the balance sheet. Cash from operations on the cash flow statement reconciles to the cash balance on the balance sheet. They're not independent documents. They're three views of the same underlying reality.

In Practice

For anyone who has run a business, none of these are academic exercises. The balance sheet is what investors are valuing. The income statement is what the board is asking about. The cash flow statement is what determines whether payroll clears next month.

What I learned is that each statement can tell a different story. A company can have strong revenue growth on the income statement while the balance sheet shows mounting liabilities. A profitable quarter can coincide with negative cash flow if clients are slow to pay. The three statements together paint the full picture. Any one of them alone can be misleading.

Why This Matters Now

I'm grounding these basics because bank financial statements follow the same framework, but the composition looks nothing like what I was used to. In a software company, assets are things like cash, equipment, and intellectual property. At a bank, the biggest asset is money that other people owe the bank. In most businesses, liabilities feel like obligations you want to minimize. At a bank, the biggest liability is client deposits, and that's the core of the business model.

The accounting framework is the same. Assets still equal liabilities plus equity. The income statement still tracks revenue and expenses. Cash flow still matters. But the structure is inverted in ways that are genuinely counterintuitive if you're coming from other industries. Understanding the general framework first makes the bank-specific version easier to navigate.